New Resolution Foundation briefing – Wages are flatlining

A new briefing from RF Chief Executive Torsten Bell and Economist Charlie McCurdy has been released today (22nd March). It examines what is happening to pay growth – a key issue as monetary policy makers decide whether to increase interest rates on Thursday.

The briefing shows that:

- Focusing on the latest headline ONS data for private sector pay growth of 6.5 per cent in the three months to January is not a good way to think about the level of wage pressure right now.

- Closer inspection shows that pay levels have stopped growing at all since November.

- This stalling of pay growth shows up not only in ONS survey data but also in HMRC’s payroll data, which shows no growth in typical pay levels between November 2022 and February 2023.

- While it’s too early to say whether this represents a decisive turn in the UK’s pay prospects, it does suggest that MPC members should worry less about wage-led inflation pressures than headline pay growth figures imply.

Charlie McCurdy, Economist at the Resolution Foundation, said:

“This Thursday, the Bank of England’s Monetary Policy Committee meets. Discussion of whether the central bank has one final rate rise in it before pausing have focused on whether the Bank’s hand will be stayed by the instability we are seeing playing out in the banking sector from Silicon Valley to Switzerland.

“But in the UK specifically something else should be more material to the MPC’s decisions – something that has gone entirely unnoticed. Wage growth has ground to a halt. Private sector pay, far from spiralling, has instead flatlined since November. The future path of wages in Britain remains very uncertain, but looking back over recent months the picture is very different from that often presented.”

This Thursday, the Bank of England (BoE)’s Monetary Policy Committee (MPC) meets. Discussion of whether the central bank has one final rate rise in it before pausing have focused on whether the Bank’s hand will be stayed by the instability we are seeing playing out in the banking sector from Silicon Valley to Switzerland (in part the result of fast rising interest rates).

But in the UK specifically something else should be more material to the MPC’s decisions – something that, oddly, has gone entirely unnoticed. Wage growth has ground to a halt, with private sector wages, far from spiralling, flatlining since November. This is now consistent across a number of months, and can be seen in separate survey and administrative data. This will be a surprise to many, but also aligns with sharp falls in firms hiring difficulties since last summer.

The future path of wages in Britain remains very uncertain, but looking back over recent months the picture is very different from that often presented: private sector pay, far from rising too fast, has not risen at all.

Labour market discussions remain focused on high annual wage growth

High pay rises, not high energy prices, are the thing most worrying some members of the MPC ahead of their meeting on Thursday. That reflects the latter falling and that the BoE’s real anxiety isn’t externally driven inflation they can do little about (from the direct and indirect effects of surging energy prices), but that this could be followed by domestically driven inflation that they very much could and should counter.

The cause of those worries is our first chart – one that dominates labour market discussions and shows strong annual nominal wage growth: regular pay growth was 6.5 per cent in the three months to January – only down slightly from the 6.7 per cent peak in the three months to December which was (the pandemic aside) the highest rate since 2000. Focusing on Figure 1, it’s hard not to conclude we’re living with a very fast pace of pay growth by any recent historical norms. Sustained wage growth of over 5 per cent is clearly not consistent with the BoE’s 2 per cent inflation target.

Figure 1 Annual pay growth is stronger than we’re used to

Annual growth in average weekly earnings (nominal terms), regular pay: GB

Notes: Growth is year-on-year change in three-month average.

Source: RF analysis of ONS, Labour Market Statistics (Average Weekly Earnings).

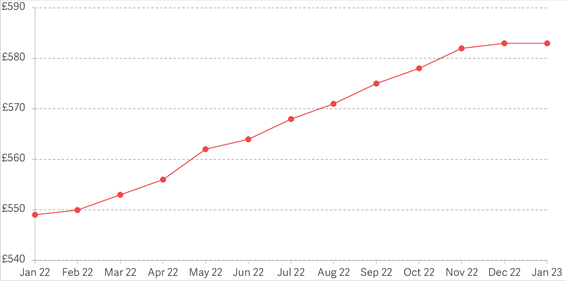

But looking instead at pay levels shows that pay growth has slowed or ground to a halt

But have private sector wages really been surging recently? No, in fact they are stalling. The key to understanding how that can be consistent with the fast annual wage growth shown above is to recognise that it matters a lot which chart you look at. Given the speed of labour market developments at present we need to look at the timeseries of the level of private sector wages (Figure 2) to interpret high annual growth rates. This allows us to see that wage growth, having been strong earlier in 2022, came to a halt from November onwards: they stood at £582 in November and £583 in January. Fast annual growth rates are telling us more about what happened yesterday than the strength of wage pressure today.

Figure 2 Average weekly earnings have stopped growing

Average weekly earnings (nominal terms), private sector: GB

Notes: Pay is regular i.e. excluding bonuses. Figures are seasonally adjusted.

Source: RF analysis of ONS, Labour Market Statistics (Average Weekly Earnings).

This analysis runs counter to much of the commentary on the labour market right now, and is a big turnaround from the experience earlier last year. So how much faith should we place in these statistics? After all this earnings data covers a relatively short space of time and is based on a survey which can be volatile. Our view on balance is that this is a turning point worth paying attention to for three reasons.

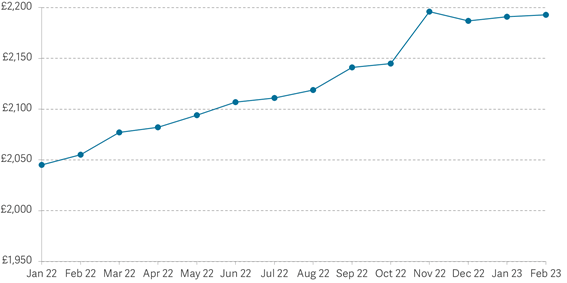

First, we’ve now seen several months’ worth of data pointing in that direction. Second, admin data is telling us exactly the same story. Figure 3 shows levels of typical monthly pay – based on HMRC’s PAYE data. Just like on Average Weekly Earnings, pay levels have not grown since November. And this timelier, if still imperfect, HMRC data also shows that stalling pay growth has continued beyond January and into February.

Figure 3 Admin data shows that pay growth has ground to a halt

Median monthly pay (nominal terms), seasonally adjusted: UK

Source: RF analysis of ONS, Pay As You Earn Real Time Information from HMRC.

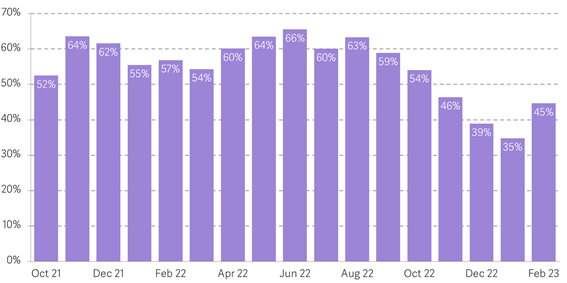

Third, pay growth slowing at the end of 2022 and into early 2023 shouldn’t really be a total surprise. Yes, people doing PR for recruitment agencies have kept repeating that the labour market is hugely tight (and that firms need to employ their services). But signs of a cooling have actually been there for all to see: firms have been clear that the exceptional hiring difficulties were over by the Autumn, as Figure 4 shows. Short term unemployment and redundancies have also picked back up to pre-pandemic norms, reinforcing this picture.

Figure 4 Hiring difficulties have eased since the summer

Proportion of businesses reporting recruitment is “much harder” than normal: UK

Notes: excludes businesses with fewer than 10 employees.

Source: RF analysis of Bank of England, Decision Maker Panel.

What the future holds on pay is very uncertain, but the deep stagnation of real wages is certainly a defining feature of our age

What the future holds on pay remains very uncertain and reasonable people will disagree. Private sector wages in several industries continue to grow. And we should see public sector pay growth strengthening in the months ahead.

There are also some signs of the economy doing better than many feared during the autumn – with the Office for Budget Responsibility last week forecasting it would avoid a technical recession this year. Consumer and firms’ reported optimism has also risen from very low levels. Pushing the other way, banks failing on both sides of the Atlantic will push down on confidence and tighten financial conditions facing businesses and households.

What is clear is that BoE policy makers should not think of today’s labour market as being the same as that of last summer – or indeed the same as the United States where concerns about entrenched wage pressure and inflation have far more empirical grounding.

For us, the middle of 2022 may best be thought of as the result of a very particular combination of surging inflation and post-pandemic reopening. In that view, exceptionally high pay growth then may reflect the one-off contest between capital and labour for how the pain of Britain getting poorer from rising energy costs was to be born, rather than the structural change to worker power than some of the more breathless commentaries implied.

After all the big picture is that recent high inflation has driven a fall in real wages that compounds, but very much didn’t begin, the unprecedented 15-year stagnation in British living standards we’re living through. Real wages have not grown since the financial crisis, leaving real average weekly earnings around £11,000 per year lower than they’d have been had previous growth rates continued. The future may be uncertain, but we should be clearer eyed about the past: wages, far from surging, have flatlined in recent months.

Responses